California Dream For All Down Payment Assistance: Pros & Cons

California Dream For All Down Payment Assistance: Pros & Cons

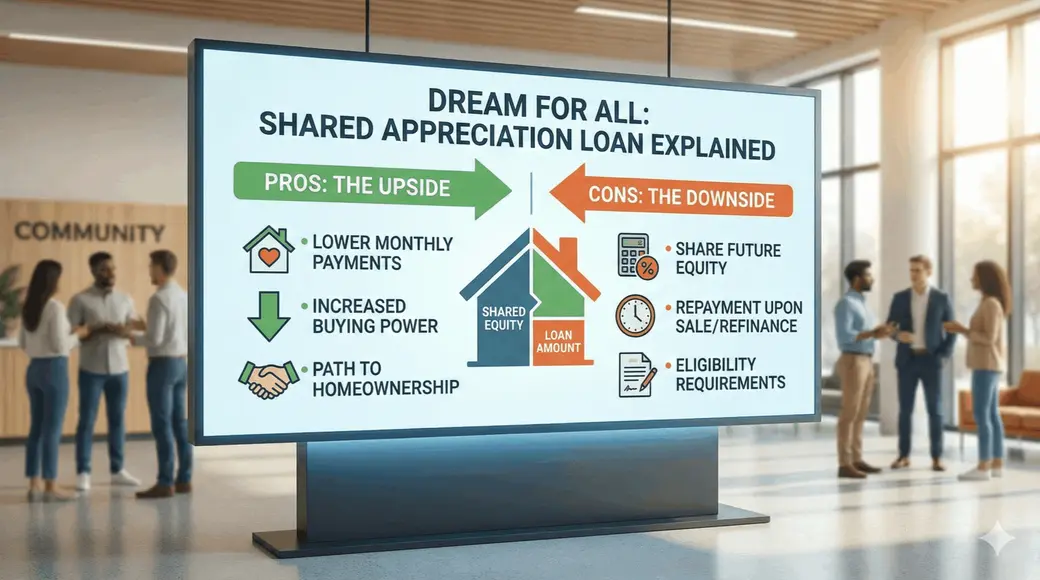

California is reopening Dream For All, a CalHFA program that can cover up to 20% of a home’s purchase price (capped at $150,000) for eligible buyers—but it’s not “free money.” It’s a shared appreciation loan, meaning you repay the assistance later plus a share of your home’s appreciation.

For San Diego County buyers, this program can be the difference between staying on the sidelines and getting into the market—if you understand the trade-offs before you sign up.

What is Dream For All?

Dream For All is a down payment and/or closing cost assistance program administered by the California Housing Finance Agency (CalHFA). The state expects demand to exceed funding, so the program uses a randomized selection (lottery-style) process rather than “first come, first served.”

Key headline details

-

Assistance amount: Up to 20% of purchase price, max $150,000

-

Application window (current cycle): Feb. 24, 2026 through 5 p.m. PT March 16, 2026

-

Repayment: repay the original assistance plus a share of appreciation when you sell/transfer/refinance/pay off the first mortgage

Who qualifies (and who doesn’t)

Dream For All is targeted. In plain English: it’s designed for first-time, first-generation California buyers who meet county income limits.

Baseline eligibility you should expect

-

First-time homebuyer (generally not owning in the last few years)

-

First-generation homebuyer (CalHFA has used a stricter definition—example described as not owning for 7 years and parents not currently owning a home)

-

California resident (at least one borrower)

-

Meet county income limits

San Diego County income limit (Dream For All income limits list): $207,000 (effective 2025 schedule in CalHFA’s posted limits document).

Reality check: Even with higher income limits in some counties, funding is limited. A recent cycle saw ~2,000 vouchers issued from ~18,000 eligible applicants, which tells you the odds can be competitive.

How the shared appreciation payback works (simple version)

This is the part buyers gloss over—and it’s the part that matters most.

When you eventually sell (or refinance, or otherwise trigger payoff), you typically repay:

-

The original down payment assistance amount, plus

-

A share of your home’s appreciation, commonly described as:

-

Up to 20% of appreciation if your income is above 80% of AMI

-

Up to 15% of appreciation if your income is at or below 80% of AMI

Quick example (rounded numbers)

-

Purchase price: $800,000

-

Dream For All assistance: 20% = $160,000 → capped at $150,000

-

You sell later for: $950,000

-

Appreciation: $150,000

-

You repay: $150,000 + (15%–20% of $150,000 = $22,500–$30,000)

That’s not “bad.” It’s the cost of getting into the market sooner—without writing a massive down payment check up front.

Pros of Dream For All (why buyers like it)

This program solves the hardest part of buying in coastal California: the upfront cash.

Key benefits

-

Massive down payment help (up to 20%, capped at $150,000) can reduce your first mortgage amount

-

Potential to avoid mortgage insurance if your total down payment structure reaches conventional thresholds (scenario-dependent)

-

Can make your monthly payment more manageable by borrowing less (CalHFA has cited meaningful monthly savings in program discussions)

-

Structured to recycle funds back into future rounds (shared appreciation repayment model)

San Diego angle: In a market where many listings still price like a “premium zip code,” the buyers who win are often the ones who can act fast with financing lined up. Dream For All can be a leverage tool—if you’re prepared.

Cons of Dream For All (the trade-offs you need to accept)

This program is powerful—but it comes with real constraints.

Main drawbacks

-

You give up part of your future upside. That shared appreciation payment can be meaningful if the home appreciates strongly.

-

It’s not guaranteed. Selection is randomized, and demand can dwarf supply.

-

Timing pressure. The window is limited (Feb. 24–March 16, 2026 in this cycle).

-

Rules matter. You’ll need to follow the program’s lender/loan structure requirements and document eligibility carefully.

Market risk note (practical, not hype): If prices dip after you buy, you still owe the principal amount you borrowed. That’s true of any down payment loan—but it’s especially important to understand when you’re using assistance to buy sooner.

Search homes for sale in San Diego HERE

How to get ready (San Diego buyer playbook)

If you’re considering Dream For All, don’t start with the lottery. Start with your financing readiness.

Do this first

-

Pull your income documents and confirm you’re under the San Diego County limit ($207,000)

-

Talk to a lender who actually originates CalHFA-style programs (not every lender does)

-

Know your target neighborhoods and property types (condo vs SFR affects HOA budgets, insurance, and approvals)

-

Decide your “walk-away” criteria (payment ceiling, commute, HOA max, inspection red flags)

Do this next

-

Enter the portal/registration during the open window and follow the rules carefully

Local strategy tip: San Diego buyers who succeed tend to have two plans:

-

a Dream For All path, and

-

a backup option (City/County programs, seller credits, smaller down payment conventional, etc.). The San Diego Housing Commission and County-administered programs can also help certain buyers—often with different income caps and property rules.

Bottom line for San Diego County

California Dream For All down payment assistance can be a smart move if:

-

you’re otherwise payment-qualified,

-

you’re short on down payment cash,

-

and you’re comfortable sharing a piece of appreciation later.

If you’re planning to hold long-term, the trade-off may be worth it. If you expect to refinance quickly or sell in a few years, run the math carefully.

FOLLOW THIS LINK TO READ ON HOW TO REGISTER.

CTA: If you want, I can help you pressure-test this with real San Diego numbers—purchase price targets, HOA scenarios, and what the shared appreciation could look like in best- and worst-case outcomes. Schedule a buyer strategy call

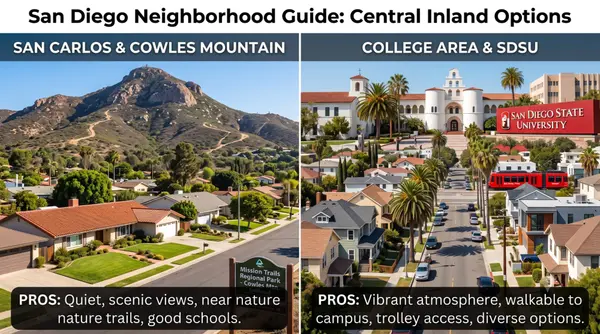

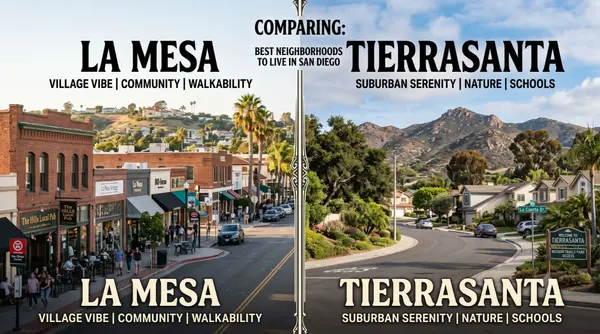

San Diego neighborhoods where Dream For All may pencil

Dream For All down payment assistance can “pencil” best where purchase prices stay under your payment ceiling and you can find condos/townhomes with HOAs that don’t blow up the monthly. In San Diego County, that often means condo-heavy pockets and attached-home submarkets with deeper inventory.

Condo-heavy areas that buyers commonly target

-

Clairemont (especially condo communities near Balboa/Genesee corridors): Central location, often better value than coastal zips.

-

Mira Mesa: Large pool of townhomes/condos and steady demand from local employers.

-

Serra Mesa: Smaller condo inventory, but sometimes more attainable pricing than neighboring areas.

-

Kearny Mesa: Pockets of condos near employment hubs; commute-friendly for many buyers.

-

Mission Valley: High concentration of condos; you’ll want to watch HOA and special assessments closely.

-

University City (select condo tracts): UCSD-adjacent demand supports resale, but pricing can vary block to block.

-

Rancho Bernardo (condos/55+ adjacent options): Some attached-home communities can offer relative value for north inland buyers.

-

Chula Vista (west + some east condo communities): More attached inventory; often more budget-friendly than central San Diego.

-

National City: Attached homes and condos can be more attainable; verify building financing eligibility early.

-

La Mesa & El Cajon (condo pockets): More inventory at lower entry points; HOA and insurance costs still matter.

Where the math can break quickly (watch these)

-

High-HOA luxury towers (often Downtown): Great lifestyle, but HOAs can push DTIs past lender limits.

-

Older condo complexes with deferred maintenance: special assessments can hit after you’re in escrow.

-

Coastal condo submarkets (PB, OB, parts of Encinitas/Carlsbad): price-per-square-foot can outpace what the program solves.

Local underwriting reality checks (don’t skip)

-

Ask your lender to review HOA dues + insurance up front. This is where “pencils” usually fails.

-

Confirm the building is warrantable/financeable (some condos run into lending restrictions).

-

Price your offer with the shared appreciation payback in mind—especially if you expect a shorter hold period.

FAQ: California Dream For All Down Payment Assistance (San Diego Focus)

1) What is the California Dream For All down payment assistance program?

Dream For All is a CalHFA shared appreciation loan that can provide up to 20% of the purchase price (max $150,000) for down payment and/or closing costs. Repayment happens later, with a share of appreciation.

2) When can I apply for Dream For All in 2026?

For the current cycle, the pre-registration portal opens February 24, 2026 and closes 5 p.m. PT on March 16, 2026.

3) Is Dream For All first-come, first-served?

No. CalHFA anticipates demand will exceed funding and uses a randomized selection process.

4) Who qualifies as a first-generation homebuyer?

CalHFA has described first-generation as a buyer who has not owned in the last 7 years and whose parents do not currently own a home (with additional details for deceased parents). Always verify your exact eligibility with an approved lender.

5) What is the income limit for Dream For All in San Diego County?

CalHFA’s published Dream For All income limits list shows San Diego County: $207,000 (effective 2025 schedule).

6) How much do I pay back with Dream For All?

You generally repay the original assistance amount plus a share of your home’s appreciation when the home is sold/transferred or the first mortgage is paid off. Many summaries describe the appreciation share as up to 15% or up to 20%, depending on income relative to AMI.

7) What triggers repayment of the Dream For All loan?

Common triggers include selling or transferring the home, and paying the first mortgage in full (which can include certain refinances).

8) How competitive is Dream For All?

It can be very competitive. A recent cycle referenced about 2,000 vouchers issued out of about 18,000 eligible applicants.

9) Does Dream For All work anywhere in California, including San Diego?

Yes. Reporting on the program notes it’s available statewide (no specific geographic requirement), assuming you meet eligibility and income limits for the county where you buy.

Chris Melingonis - The Realtor Dad

With almost two decades of experience in the real estate market, I have dedicated my career to helping families buy and sell homes in La Mesa and San Diego, California. My extensive knowledge of the local market allows me to provide valuable insights and guidance, ensuring my clients feel confident and informed throughout the entire process. I understand that real estate transactions can be daunting, which is why I prioritize education and clear communication to help my clients navigate even the most challenging situations.

My unique marketing plan is designed to get homes sold quicker and at maximum value. By leveraging cutting-edge technology and innovative strategies, I showcase properties in a way that attracts potential buyers and stands out in the competitive San Diego market. I am committed to using my experience to tailor my approach to each client's specific needs, ensuring a seamless experience from start to finish.

Whether you are a first-time homebuyer or looking to sell your cherished property, I am here to guide you every step of the way. My focus on building lasting relationships and providing exceptional service has earned me the trust of many families in our community. Together, we can make your real estate dreams a reality.

Recent Posts